Ever picked up your prescription and been shocked by the price? You thought you were getting a generic drug-cheaper, same medicine, right? But your copay was $45 instead of $5. You’re not imagining it. This isn’t a mistake. It’s the system.

What Exactly Is a Tiered Copay System?

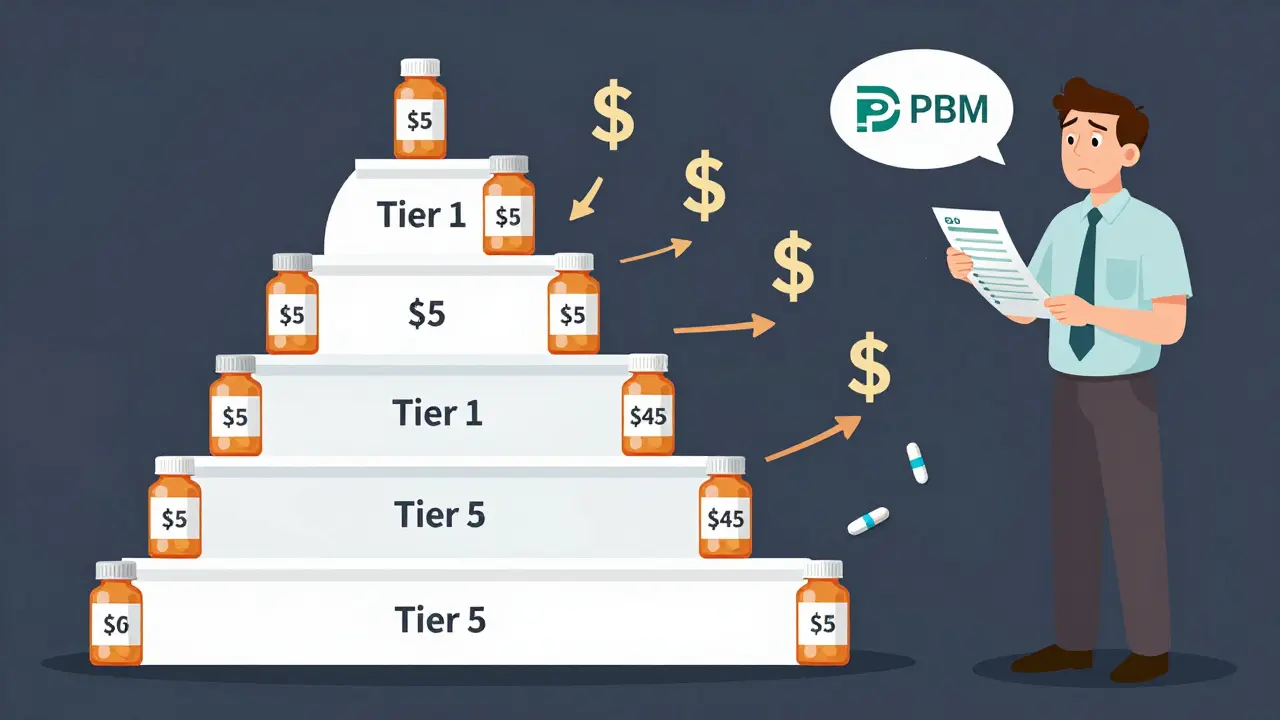

Most health plans today don’t charge the same amount for every prescription. Instead, they use a tiered system. Think of it like a pricing ladder. The lower the tier, the less you pay. Tier 1 is usually for the cheapest drugs. Tier 2 and 3 are for more expensive ones. Tier 4 and 5? Those are for specialty drugs-often the ones that cost thousands a month.But here’s the twist: not all generics are in Tier 1. Some generics, even ones that are chemically identical to their cheaper cousins, sit in Tier 2 or even Tier 3. That means you pay more-sometimes double or triple-just because your insurer’s contract with the manufacturer changed.

Why Would a Generic Be in a Higher Tier?

You’d think all generic versions of a drug are treated the same. After all, they contain the exact same active ingredient. But that’s not how it works.Insurers don’t pick tiers based on how well a drug works. They pick based on money. Specifically, how much rebate the drugmaker gives to the Pharmacy Benefit Manager (PBM)-the middleman that negotiates prices for your plan.

If a manufacturer offers a big enough discount, their generic gets placed in Tier 1. If they don’t? It gets bumped up. Even if it’s the same pill, same dosage, same manufacturer. It’s not about quality. It’s about the deal.

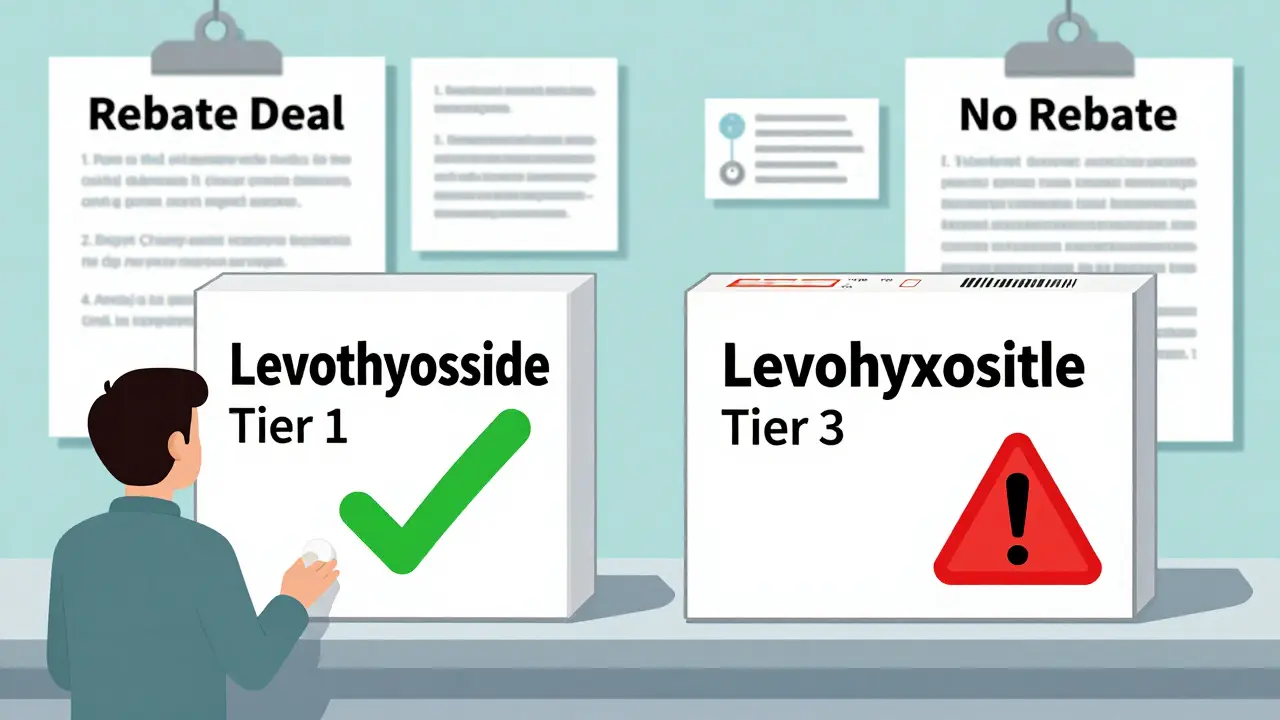

Take levothyroxine, a common thyroid medication. One generic version might cost $5. Another, made by a different company but with the same ingredients, might cost $45. Why? The first one has a strong rebate deal. The second doesn’t. Your plan only covers the cheaper one at the low rate.

How This Hurts Patients

This system creates real problems. Patients get confused. They think they’re getting the same drug, so why pay more? Some switch back and forth between generics, not realizing they’re the same. Others just stop filling prescriptions because the cost jumps unexpectedly.Studies show this leads to worse health outcomes. When a drug moves from Tier 1 to Tier 3, adherence drops by over 7%. That’s not just about money-it’s about trust. If you can’t understand why your medication suddenly costs more, you stop taking it.

And it’s not rare. A 2023 survey found 41% of insured adults had a generic drug move to a higher tier without warning. Over half said their insurer gave no clear reason why. That’s not customer service. That’s a design flaw.

Specialty Generics Are the Worst

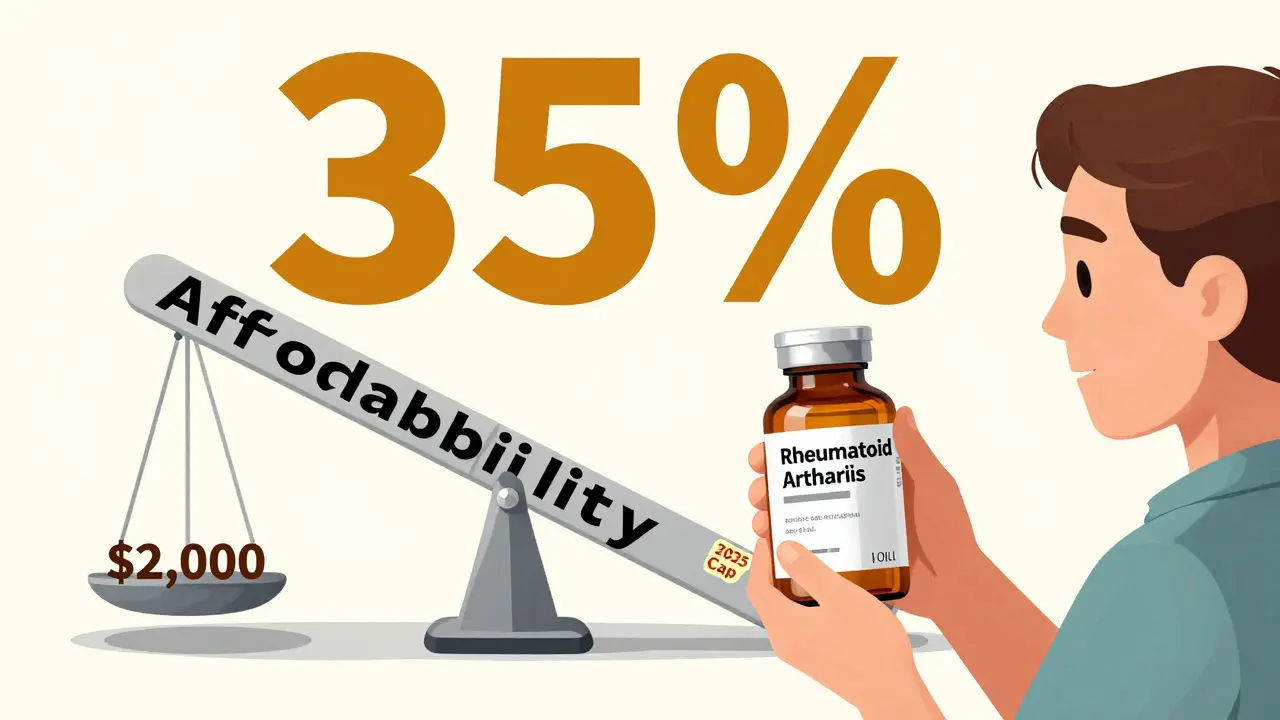

The biggest pain point? Specialty generics. These are generic versions of expensive biologic drugs-like those used for rheumatoid arthritis, multiple sclerosis, or Crohn’s disease.These drugs used to cost $5,000 to $10,000 a month. Now, generics are available. But they’re still placed in Tier 4 or 5. Why? Because even though they’re cheaper than the brand, they’re still expensive to make. So insurers slap a 25-40% coinsurance on them. That means you pay thousands out of pocket, even if you have insurance.

And here’s the kicker: sometimes, the generic version is the only option. No brand-name alternative exists. So you’re stuck paying a huge percentage of a high price-even though it’s technically a generic.

How to Navigate This Mess

You can’t change the system. But you can work around it.- Check your formulary every year. Plans update them in October. What was Tier 1 last year might be Tier 2 this year.

- Use tools like GoodRx or SmithRx. They show you price differences between generics and even suggest alternatives.

- Ask your pharmacist. Pharmacists know which generics are preferred. They can often switch your prescription to a lower-tier version without a new doctor’s note.

- Request a therapeutic interchange. Your doctor can submit a form asking your insurer to cover a non-preferred drug because it’s medically necessary. Success rate? Around 63%.

- Look for manufacturer assistance. Many drugmakers offer discount programs or coupons-even for generics. Check their websites.

And if you’re hit with a surprise price hike, file an appeal. Most plans have a 72-hour window for urgent cases. Don’t assume it’s hopeless. People win these appeals all the time.

What’s Changing in 2025 and Beyond?

The Inflation Reduction Act kicks in next year. For Medicare Part D, your out-of-pocket drug costs will be capped at $2,000 per year. That’s huge. But it doesn’t eliminate tiered copays. It just limits how much you pay after hitting that cap.Some PBMs are already adjusting. UnitedHealthcare moved several high-volume generics (like atorvastatin) to $0 copays in 2024. Others are moving less common generics to higher tiers to make room.

But the core problem remains: tier placement is still based on rebates, not patient need. And until that changes, you’ll keep seeing the same pattern-your generic drug costs more because the rebate expired, not because it’s any different.

Bottom Line

Your generic isn’t being priced fairly. It’s being priced based on a contract between a drugmaker and a middleman you’ve never heard of. That’s not transparency. That’s a hidden tax.The system was built to save money. And it did-for insurers and PBMs. But patients are paying the price-in confusion, skipped doses, and higher bills.

Know your plan. Ask questions. Push back. And don’t assume your pharmacist or doctor has all the answers. This isn’t about medicine. It’s about money. And you deserve to know why you’re paying what you’re paying.

11 Comments