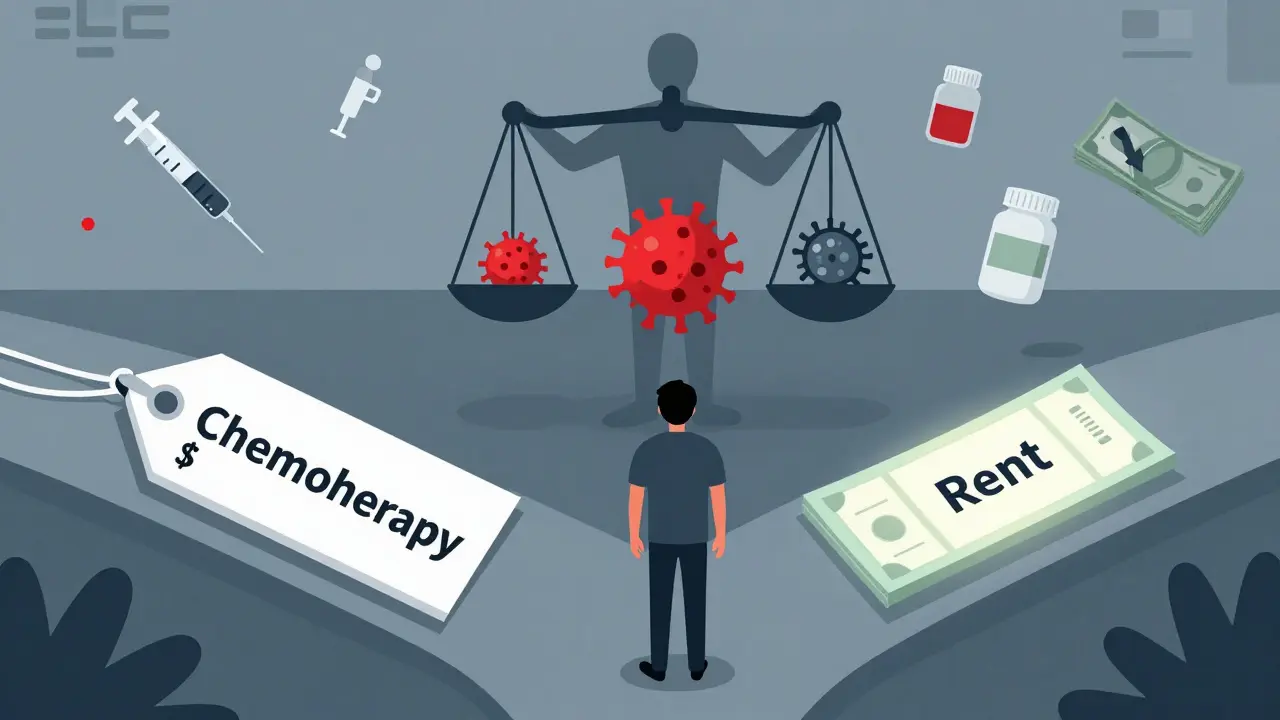

When someone is diagnosed with cancer, the fear isn’t just about the disease-it’s also about the bill. Financial toxicity isn’t a buzzword. It’s the real, daily stress of choosing between buying insulin and paying for chemotherapy, between keeping the lights on and filling a prescription. This isn’t about being poor. It’s about how cancer care, even in wealthy countries, has become a financial trap for millions.

The term was coined in 2013 by researchers at Duke University, but it didn’t become widely known until cancer survivors started speaking up. One woman in her 40s, diagnosed with breast cancer, told her oncologist she was skipping doses because her copay was $450 every month. She worked two jobs. She had two kids. Her insurance had a $7,000 deductible. She wasn’t alone. Studies show that 28% to 48% of cancer survivors face measurable financial hardship. For some, it’s worse: low-income women with breast cancer spend up to 98% of their annual income just on treatment.

What Exactly Is Financial Toxicity?

Financial toxicity isn’t just about medical bills. It’s the full weight of everything cancer costs-direct and hidden. Direct costs include copays, deductibles, premiums, and the price of drugs. A single cycle of immunotherapy can cost $10,000 to $15,000. Some treatments last years. One patient I spoke with (name changed for privacy) was on a targeted therapy for 37 months. Her out-of-pocket costs totaled $186,000. Even with insurance, she paid $5,000 a month.

Then there are the hidden costs: gas to drive to appointments, parking fees, childcare during treatments, lost wages because you can’t work, and even the cost of eating well when your appetite is gone. A 2021 study found that 13% of non-elderly cancer patients spend at least 20% of their entire income on out-of-pocket cancer expenses. For Medicare beneficiaries? Half spend more than 10% of their income on cancer care alone.

The National Cancer Institute defines financial toxicity as “problems a patient has related to the cost of medical care.” That includes anxiety, debt, bankruptcy, and the shame of not being able to afford your own survival.

Who Gets Hit the Hardest?

It’s not random. Certain groups are far more likely to suffer.

- Younger patients (under 65) have less savings, fewer retirement funds, and are more likely to be underinsured. Many are still raising kids or paying off student loans.

- Low-income patients face the steepest climb. One study found that for women earning under $30,000 a year, breast cancer treatment wiped out nearly all their income.

- Patients with metastatic cancer are stuck in long-term treatment. A drug that works for years means paying for it for years. Immunotherapy and targeted therapies-while life-extending-are also the most expensive.

- Underinsured patients are the most vulnerable. High-deductible plans sound good on paper until you need $200,000 in care. Then your deductible becomes a wall.

Even patients in clinical trials aren’t safe. A 2023 study found that 82% of patients in phase 1 trials reported medical cost concerns. 79% said they felt financial stress. These are people getting cutting-edge care-and still drowning in bills.

The Real Cost: More Than Money

Financial toxicity doesn’t just hurt wallets. It kills.

Patients who are financially stressed are more likely to:

- Skip doses or stop treatment because they can’t afford it

- Delay scans or follow-ups

- Go without food, heat, or medication to pay for cancer care

- Report higher levels of depression, anxiety, and pain

In one study, patients said financial toxicity felt “more severe than physical, emotional, or family distress.” That’s not hyperbole. One man in Wisconsin told his nurse he’d rather die than let his wife lose their home. He didn’t want to talk about his tumor. He wanted to talk about his mortgage.

And it doesn’t end when treatment stops. Survivors often face long-term side effects-nerve damage, heart problems, secondary cancers-that require ongoing care. A 2023 NCI report found that many survivors still struggle with medical debt five years after diagnosis.

What’s Being Done?

Some progress is happening-but it’s uneven.

Financial navigation programs are one of the most effective tools. These are trained staff-often social workers or patient advocates-who help patients find grants, apply for assistance, and understand insurance. One 2022 study showed that hospitals using these programs cut treatment abandonment due to cost by 30-50%.

The Patient Advocate Foundation gave $327 million in copay assistance to 67,000 cancer patients in 2022 alone. Pharmaceutical companies provided $12.8 billion in aid to 1.8 million patients. But here’s the catch: many patients don’t know these programs exist. Or they’re too sick to fill out forms. Or they’re turned away because their income is “too high” for aid but still can’t afford care.

Some states are stepping in. California’s 2022 Cancer Drug Affordability Act requires drugmakers to justify price hikes and report costs to the state. Other states are looking at similar laws. The Cancer Drug Parity Act, reintroduced in 2023, would force insurers to charge the same copay for oral drugs as for IV treatments-something that’s currently not true. Oral drugs are often more expensive because patients pay retail, not bulk.

Screening is changing too. The American Society of Clinical Oncology now recommends routine financial toxicity screening for all patients. Tools like the Comprehensive Score for Financial Toxicity (COST) ask simple questions: “Have you skipped doses due to cost?” “Have you cut back on food or heat?” “Are you worried about paying bills?” Mayo Clinic found that using these tools increased detection of at-risk patients by 45%.

The Future: What Needs to Change

There’s no fix that’s quick or easy. But here’s what’s working-and what’s not.

AI is helping. A 2023 study in JAMA Internal Medicine used machine learning to predict which patients would face financial toxicity with 82% accuracy. It looked at age, income, insurance type, cancer stage, and treatment plan. This isn’t sci-fi. It’s already being tested in clinics. Imagine a doctor seeing a red flag on the screen: “High risk for financial toxicity. Connect to navigator.” That’s the future.

Insurance needs reform. High-deductible plans are a disaster for cancer patients. A $10,000 deductible doesn’t make sense when your treatment costs $200,000. Experts are pushing for caps on out-of-pocket costs for cancer care-something like the $10,000 annual cap for Medicare beneficiaries.

Drug pricing is the elephant in the room. The U.S. spends more on cancer drugs than any other country. A 2023 report found that the average cost of a new cancer drug in the U.S. is $150,000 per year. In Canada? $40,000. In Australia? $35,000. Why? Because we don’t negotiate prices. Other countries do. We need to.

By 2025, experts predict 75% of NCI-designated cancer centers will have formal financial toxicity screening programs. That’s up from 35% in 2022. Progress. But it’s still not standard everywhere.

What Can You Do?

If you or someone you love is facing cancer:

- Ask for a financial navigator. Every major cancer center has one. Don’t wait until you’re overwhelmed.

- Ask about patient assistance programs. Even if you think you make “too much,” apply. Many have sliding scales.

- Know your insurance. Call your insurer. Ask: What’s my copay for this drug? What’s my out-of-pocket maximum? Do I need pre-authorization?

- Don’t be afraid to talk about money. Say: “I can’t afford this.” Your care team can help. They’ve seen this before.

- Check state programs. Some states offer financial aid for cancer care. California, New York, and Washington have active programs.

- Keep records. Save every bill, every explanation of benefits. You’ll need them for appeals or aid applications.

Financial toxicity isn’t your fault. It’s a system failure. But you don’t have to fight it alone. Help exists. You just have to ask for it.

What is financial toxicity in cancer care?

Financial toxicity is the financial burden and emotional distress caused by the cost of cancer treatment. It includes out-of-pocket expenses like copays, deductibles, and drug costs, as well as indirect costs like lost wages, travel, and childcare. It’s recognized by the National Cancer Institute as a serious side effect of cancer care that can lead to treatment delays, debt, and worse health outcomes.

How common is financial toxicity among cancer patients?

Studies show that between 28% and 48% of cancer survivors experience measurable financial hardship. When self-reported, the numbers rise to 16%-73%. One in seven non-elderly patients spends at least 20% of their income on cancer care. For low-income women with breast cancer, treatment can consume up to 98% of their annual income.

Why are newer cancer treatments more expensive?

Newer therapies like immunotherapy and targeted drugs are often developed by private companies and priced to maximize profit. A single year of treatment can cost $150,000 or more. These drugs may extend life by months or years, but they’re rarely cheaper than older chemotherapy. Unlike in other countries, the U.S. doesn’t negotiate drug prices, so costs stay high.

Can financial toxicity affect cancer survival?

Yes. Patients who skip doses, delay scans, or stop treatment because they can’t afford it are more likely to have worse outcomes. Studies link financial stress to higher rates of hospitalization, faster disease progression, and increased mortality. Financial toxicity is now considered as serious a side effect as nausea or fatigue.

What help is available for cancer patients struggling with costs?

Many options exist: financial navigators at cancer centers, patient assistance programs from drugmakers (like Pfizer’s and Roche’s), nonprofit organizations like the Patient Advocate Foundation, state-level aid programs, and copay relief funds. Medicare and Medicaid also have limits on out-of-pocket spending. The key is to ask early-don’t wait until you’re in crisis.

15 Comments